Buying Power Calculator: Find Out What Your Money Is Really Worth

| Year | Future Value | Power Lost | % Lost | Real Value |

|---|

Buying Power Calculator: Find Out What Your Money Is Really Worth

You earn money. You save money. But every year, that money quietly loses strength—even when the number in your account stays the same. That is inflation working against you, and most people do not notice it until it has already done serious damage.

This buying power calculator gives you a clear, honest picture. Enter your amount, set an inflation rate, and pick a time. In seconds, you will see the future value you need to maintain the same lifestyle—and exactly how much purchasing power you are likely to lose along the way.

What Is a Buying Power Calculator?

A buying power calculator estimates how much more money you will need in the future to afford what you can buy today. It takes a starting amount, an annual inflation rate, and several years and then compounds that rate over time to show you the real financial gap.

This is different from a basic savings calculator. It does not measure how your money grows. It measures how inflation quietly reduces what your money can actually buy—which is the number that matters most for real-life planning.

Why Your Account Balance Does Not Tell the Whole Story

Most people watch their savings balance. Very few track their real buying power. But the balance alone tells you nothing about whether you are genuinely ahead or silently falling behind.

When prices rise faster than your income or savings grow, your real wealth shrinks—even if the number in your account stays the same or grows slightly. You still have the money, but it stretches less far every single year.

Knowing your buying power can help you set better savings goals, negotiate better raises, and create financial plans that can truly weather rising prices.

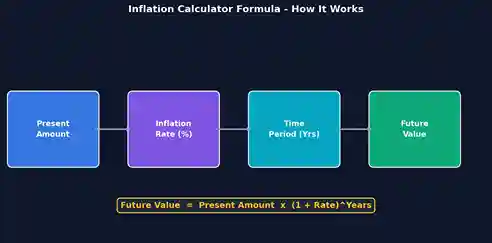

The Formula Behind the Calculator

The tool uses compound inflation—the same principle that makes compound interest powerful, but working against you.

Future Value = Present Amount x (1 + Inflation Rate) ^ Years

Each year’s price increase builds on the previous year’s already-higher price level. That is why inflation feels slow at first and much more serious after a decade or two. A low annual rate does not add up linearly—it compounds.

If you choose more frequent compounding (monthly or quarterly), the calculator divides the annual rate by the number of periods and adjusts the years accordingly. This gives a slightly higher future value, especially for longer periods of time.

How to Use This Inflation Impact Calculator

Step 1: Enter the Present Amount

Start with the amount you want to test. Enter the present amount you’re saving, your monthly expenses, your annual salary, school fees, or any other costs you want to compare against future inflation. The calculator treats the amount as your starting point in today’s money.

Step 2: Set the Annual Inflation Rate

Enter the inflation rate you expect. Use a current estimate, a long-term historical average, or a stress test number to see how different inflation levels could affect your budget. Running a few different rates provides you a range of outcomes instead of one fixed guess.

Step 3: Choose the Time

Select how many years you want to project. Shorter periods work well for near-term budgets. The longer you look out, the more you see the real effects of inflation on saving for retirement and paying for education and other long-range financial goals.

Step 4: Read and Act on the Results

After you calculate, review the future value needed, total purchasing power lost, percentage of value eroded, real value in today’s terms, and the year-by-year breakdown table. Each number answers a different planning question—so do not just look at the headline figure.

What Each Result Actually Means

Future Value Needed

This answers the question: How much money will I need later to buy what this buys today? It is the most important number for savings goals, salary benchmarks, and future expense planning.

Purchasing Power Lost

It’s the difference between the initial amount and its real value at the end of the period (in today’s money). It makes the erosion feel real because you can compare it side by side with what you started with.

Percentage Loss

Shows how much of your original buying power you lose during your period of choice. It’s a quick way to compare different inflation rates or times without getting lost in dollar amounts.

Real Value Today

This calculation translates future erosion back into today’s terms. It shows what your current amount will effectively feel like after inflation has run for the full period—a useful way to grasp long-term value loss.

Year-by-Year Breakdown

The table shows how purchasing power declines step by step across each year. Inflation does not feel dramatic in year one, but by year ten or fifteen, the cumulative effect becomes impossible to ignore.

How This Calculator Helps With Savings Planning

Savings can lose real value even when the balance grows—if that growth is slower than inflation. A savings account returning 2% per year in a 6% inflation environment is still a losing position in real terms.

Use this calculator to assess the difference between your savings and your actual needs. It helps you set more realistic emergency fund targets, education savings goals, retirement estimates, and large purchase budgets.

The break-even return result shows the minimum annual return needed to at least keep pace with inflation. That is not a performance guarantee—but it gives you a clear benchmark to plan around.

Why Salary Planning Needs Inflation Awareness

A raise looks good on paper. But if inflation rises at the same rate or faster, your real income stays flat or actually falls. Many employees accept offers without considering what the purchasing power of that salary will feel like in three or five years.

The salary tracker estimates how much your income needs to grow just to maintain the same lifestyle. It breaks down the monthly raise needed over your chosen period—a useful figure to bring into a salary review, a freelance pricing discussion, or a contract renewal.

Business owners can use the same feature to check whether current rates still reflect real costs—or whether pricing needs to adjust to keep up with rising expenses.

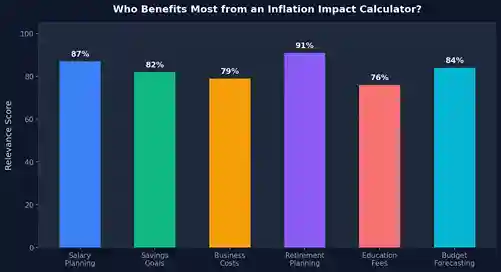

Who Should Use This Calculator?

If you want to plan with real numbers (not just nominal), this tool can be valuable to you.

- Employees preparing for a salary review or evaluating a job offer.

- Families budgeting for rent, groceries, or school fees.

- Contractors are looking at long-term pricing and contract rates.

- Business owners who want to plan future operating expenses and profit margins.

- Students estimate future tuition or living costs.

- Retirees wondering whether their fixed income keeps pace with rising prices.

- People who have savings and want to understand real growth vs. inflation.

Everyday Examples of Inflation Impact

Linking inflation to real spending makes it easier to understand. A monthly grocery bill, utility cost, fuel expense, or rent payment shows how quickly small annual increases add up.

If your grocery spend is $500 per month today, at 6% annual inflation, it becomes roughly $895 per month after 10 years, with no change in the amount of food you buy. That is nearly $400 extra per month to maintain the same basket.

The calculator’s everyday buying power examples help you relate abstract percentages to real purchases, making the results more actionable and easier to discuss with a partner, employer, or financial adviser.

Inflation and the Cost of Living

When the price of basic things like food, housing, transport, health, education, and utilities increases, the cost of living increases too. But inflation isn’t the same for all households. Your personal inflation rate will depend on what mix of spending you have.

A household that spends heavily on rent feels the effects of housing inflation first. A commuter feels fuel prices faster. A parent feels school fee increases earlier. This calculator lets you test your specific amounts rather than relying on a national average that may not reflect your life.

Understanding CPI and How It Connects to This Tool

The Consumer Price Index, or CPI, measures the change in price of a basket of common goods and services. Central banks and policymakers use this data to set interest rates and guide monetary policy.

This inflation impact calculator works differently. It lets you choose your rate and test your amounts—so you can model personal scenarios, not just follow headline economic data. For historical comparisons, use an official CPI tool. Use this calculator to plan.

Historical Inflation vs. Future Inflation - Which One Matters More?

Both are important, but they answer different questions.

Historical inflation compares money over past years using recorded data. Future inflation assumes a rate and calculates what your money will need to be. This tool focuses on future inflation—the kind that is relevant for decisions you are making right now.

How Compounding Makes Inflation More Powerful Than It Looks

Compounding is the reason inflation feels manageable in the first year but punishing after a decade. At 5% inflation, prices do not rise by just 50% after 10 years—they rise by about 63%, because each year’s increase builds on the previous year’s already-higher base.

The calculator handles all compounding automatically. You just enter your numbers and get the full compound result—no manual formula required.

The Rule of 72: A Quick Inflation Shortcut

To estimate how long it would take for purchasing power to halve, divide 72 by your annual rate of inflation. At 6% inflation, buying power roughly halves in 12 years. At 3%, it takes about 24 years. The calculator displays this figure alongside your results as a quick way to compare different rates.

Testing Scenarios Before Big Financial Decisions

The best financial decisions account for a range of possible futures—not just one assumed rate. The scenario comparison feature lets you test a low, base, and high inflation scenario side by side so you can see how sensitive your plan really is.

A financial plan that works at 3% inflation may feel entirely unique at 7% or 10%. Scenario testing reveals where you need more cushion and which goals are most vulnerable to rising prices.

Using This Calculator for Business Budgets

Businesses face inflation on multiple fronts at once—supplies, wages, rent, utilities, software, shipping, and raw materials can all move at different rates.

A business owner can enter current operating expenses and test how different inflation rates affect the total over three, five, or ten years. The year-by-year table shows when cost pressures may become hard to absorb without a pricing adjustment—making budget planning more proactive and less reactive.

Common Mistakes to Avoid When Using Inflation Calculators

Treating the Result as a Guarantee

The calculator gives estimates based on your inputs. Actual inflation varies year to year and differs across spending categories. Use the result as a planning range, not a fixed prediction.

Using Only the Headline Rate

If you primarily spend on housing, food, or healthcare, those categories tend to outpace the average CPI. Use a rate that shows how you actually spend to get a more accurate picture.

Ignoring Compounding

A 5% annual rate does not mean 50% in 10 years. The actual impact is higher due to compounding. Always use the compound result the calculator provides—not a simple multiplication.

Tips for Getting the Most Accurate Results

- Use a realistic inflation rate. For extreme inputs, you can obtain outputs that are unlikely to happen.

- At least run three scenarios (conservative, base, aggressive). This gives you a planning range instead of a single fixed answer.

- Verify your calculation from time to time. Inflation is a function of economic conditions and policy changes.

- Enter your spending amount rather than a generic figure. The more personal the input, the more useful the output.

Why This Tool Goes Further Than Basic Inflation Converters

Most inflation tools just convert one dollar amount into another. This calculator goes a step further and provides you with the future value, the lost purchasing power, the percent erosion, the salary adjustment, the minimum return required, and a year-by-year visual breakdown, all in one place.

It also handles multiple currencies and compounding frequencies, so it’s practical for a global audience. Export, Copy, Share, and Print options mean you can save results or bring them into a conversation without losing your numbers.

Best Practices for Inflation-Aware Financial Planning

Think in real value, not just nominal value. Nominal money is the number you see. Real value is what that number can actually buy—and that determines your true financial health.

Review inflation before you set long-term savings targets. What looks like a big goal today may not be so much when you consider future prices. Your targets should be based on real buying power, not account balances.

Combine inflation data with your income growth projections, expected savings rate, and realistic investment return estimates. No single number tells the whole story, but buying power is one of the most overlooked pieces of the puzzle.

Final Thoughts

Inflation does not announce itself loudly. It works quietly—shrinking the value of savings, stretching budgets tighter, and making yesterday’s salary feel smaller every year. The longer you go without accounting for it, the larger the gap becomes.

This buying power calculator puts the real numbers in front of you. Test your own amounts, run different scenarios, and build a financial picture that reflects what your money will actually be worth—not just what it says on the balance sheet.

Note

This calculator is for educational and planning purposes, not as a substitute for official economic reports or CPI data.

Frequently Asked Questions

What is a buying power calculator?

A buying power calculator will tell you how much more money you will need in the future to have the same purchasing power as today. It takes compound inflation over a period of years into account. It gives answers in simple, practical terms.

How do I calculate inflation impact?

Enter the current value, the annual rate of inflation, and the number of years. The calculator compounds the rate across each year and shows the future value needed, purchasing power lost, and a full year-by-year breakdown.

What is purchasing power?

Purchasing power is the value of your money when it comes to what it can buy. When prices rise, you are getting less for your money, so your purchasing power decreases even though your balance doesn’t.

Is this calculator for past or future inflation?

The tool is intended for future inflation scenarios. If you need to compare prices historically (e.g., what $100 in 2000 is worth today), use an official CPI calculator. This tool should be used for scenario testing and forward-looking planning.

Can I use this tool for salary planning?

Yes. Enter your current salary and an expected inflation rate to estimate how much your income needs to grow to maintain the same real purchasing power over time. to maintain the same real purchasing power over the years.

What inflation rate should I use?

For planning purposes you would use a long-term average of 3-4% and then test a higher rate of 6-8% as a stress scenario. The most accurate estimate comes by using the most recent CPI figures in your country as a benchmark.

Does the calculator give financial advice?

No. It provides educational estimates on your inputs. This can help you to plan and to understand the impact of inflation, but it is not a substitute for professional financial advice.